Peering Out onto Today's Debt Horizons and CRE State of the Market Overview:

![]()

The Distressed Asset Dilemma:

The capital market credit crunch has created significant asset value erosion since the fall of 2007. This duress has resulted in increased distressed and troubled real estate in the real property marketplace. These assets can be broken into three primary asset classifications: (a) potentially troubled assets, (b) troubled assets and (c) Lender REO (Real Estate Owned).

“Potentially Troubled” assets include maturing loans, an asset owned by an owner who is in financial trouble, assets having a troubled development or failed conversion or a failure of redevelopment, assets having a bankrupt tenant or assets which are underperforming or overvalued.

“Troubled” assets consist of delinquent or defaulted assets, assets in foreclosure or administration, assets with an owner or GP in bankruptcy, assets with maturity default or having an asset with mezzanine lender debt assumption.

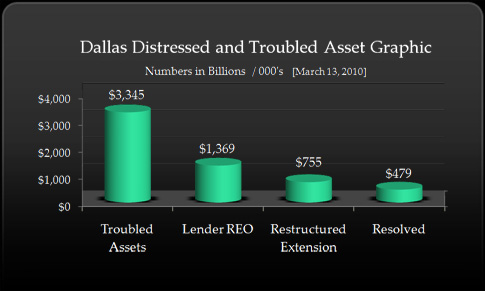

“Lender REO” includes assets in foreclosure or assets which have been returned to the mortgagee under a “deed in lieu” circumstance. A breakdown of these troubled assets is shown in the graphic above.

Through June of 2010, U.S.Troubled Assets consisted of $140.314 Billion of property. This included $22.265 Billion of Lender REO.Of that amount $22.265 Billion of these assets restructured and $21.973 Billion has been resolved.

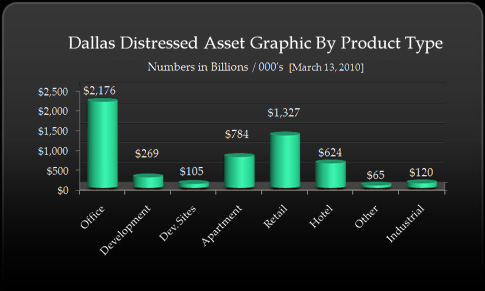

Dallas has 277 distressed assets comprising a total of value of $5,468.9 Billion. This is broken down into the following categories. includes the following category breakdown:

![]()

Industrial $ 119,000,000 [ 13 Properties ]

Retail $ 1,065,000,000 [ 62 Properties ]

Apartments $ 783,500,000 [ 65 Properties ]

Hotel $ 623,700,000 [ 38 Properties ]

Development Sites $ 374,700,000 [ 39 Properties ]

Other $ 65,200,000 [ 6 Properties ]

Totals $ 5,468,900,000 [ 277 Properties ] ![]()

Econometric Backdrops in Today's Commercial Real Estate World

![]()

Cap Rates Hit The Roof...Borrowers Hit The Fan.

The most exciting area of potential transactional activities will be found in the distressed asset category. Real estate profitability over the past decade was largely due to significant amounts of capital chasing deals.

The most exciting area of potential transactional activities will be found in the distressed asset category. Real estate profitability over the past decade was largely due to significant amounts of capital chasing deals.

Debt availability coupled with low interest rates allowed investors to procure assets with minimum amounts of equity.

Generous CMBS financing vehicles from Wall Street infused massive amounts of debt capital into the marketplace resulting in substantive cap rate compression.

This greatly expanded owner’s equity. Conversely, as the CMBS financing capabilities eroded, so too did Owner’s equity. Cap Rates on commercial properties have climbed 150-200 basis points in major property sectors and in many instances they are approaching 9-10%. This puts additional pressure on today’s individual property owners who have previously stood on the shores of “denial” hoping to avert the pervasive property value devaluation that has entered the marketplace over the last 18 months.

However, owners are going to be unable to secure new loans to fully replace their current highly leveraged underlying 1st lien mortgages which often represented 75% to 90% loan-to-value ratios. This will result in additional properties falling into the ever-increasing financially troubled asset funnel. Banks and institutional lenders will initially request their Borrowers bring a larger equity component into the deal structure. Many borrowers will not find the “risk-reward” dynamics worthy of such equity contribution and/or have the capital base and financial where-with-all to accomplish additional equity infusion.

Consequently, in an effort to get their loan portfolios in order, banks will be inclined to push delinquent borrowers into foreclosure or initiate “deed in lieu of foreclosure transactions. However, the bank’s own asset strength and capitalization structure is also be negatively impacted through these circumstances. Their capital base can be substantively eroded through “mark-to-market” accounting requisites imposed by regulators further exacerbating the situation pulling additional assets into the distressed asset category.

Asset repositioning amidst this spiraling downward market cycle is consuming both Owners and Lenders alike both of whom are trying to enhance the value of their asset portfolio base. Utilization of seasoned market-tested professionals to address these turbulent and debilitating market situations is becoming a major consideration of both prudent property owners and institutional investors.

![]()

The New Rules of Money - Rebalancing the Equity Equation

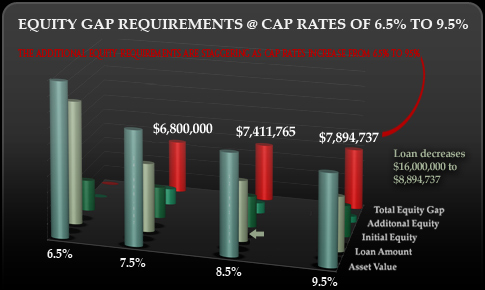

Investors are being forced to reevaluate the asset holding cost of their portfolio assets. With cap rates exploding and property values eroding, the adjusted requisite equity contribution to secure new financing is staggering. The above example contemplates an original $20,000,000 asset and a $4,000,000 equity position.

As the loan underwriters require a 65% loan to value structure, the additional equity requirement is pictured as the cap rates increase at 100 Basis Point Increases from 6.5%-9.5%. The Original Equity of $4,000,000 requires an additional capital requirement of $7,894,737 if cap rates increase to 9.5%.

More importantly the asset value decreases from its orignal $20,000,000 to $11,578,947. All investors who have refinancing requirements in the next five to seven years must evaluate whether or not such additional capital injections are appropriate as they try to optimize their portfolio holdings.

![]()